Report highlights

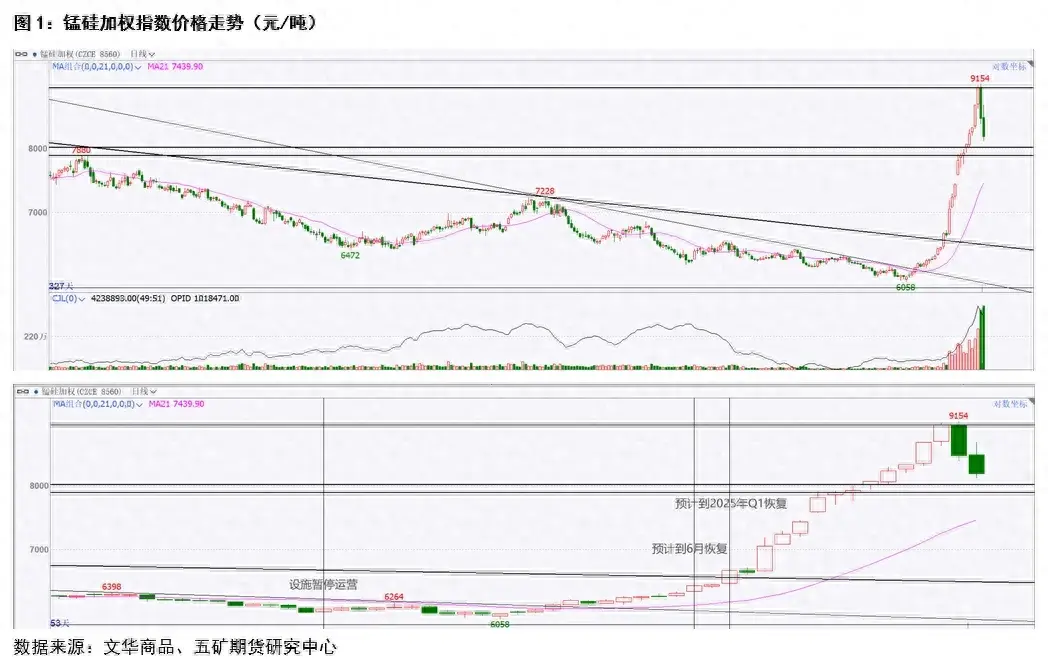

Manganese silicon futures in April rose sharply from a low of 6058 yuan/ton to a maximum of 9154 yuan/ton, a surge of 3096 yuan/ton or 51.1% in 26 trading days, becoming another eye-catching “conspicuous package” in addition to the recent European line.

Manganese silicon market drive from the manganese mining end, South32 said in its quarterly report that it is expected in the third quarter of the fiscal year 2025, that is, the first quarter of the calendar day 2025 to restart the operation and export sales of GEMCO terminal, outage events exceed market expectations, manganese ore prices “soaring”. Driven by the cost, the manganese silicon disk began to accelerate the pull up.

Although there has been a continuous sharp correction after the board rose to the heavy pressure position near 9100 yuan/ton, we see that the position of the manganese silicon board remains at an absolute high level. At the same time, we observe that although the main long positions in this rally have been reduced recently, there are still a large number of net long positions in the 09 contract. Combined with the shortage of Australian mines in the short term will not be falsified, we expect the market at the current stage or still have repeated, short-term pullback may not represent the end of the market.

Considering the large spot inventory of manganese silicon (there is a centralized cancellation of the warehouse receipt in October) and poor downstream demand, bulls expect that the real willingness to receive goods is not strong (not forced). In addition, under the catalyst of high profits, it cannot be ruled out that South32 actively seeks alternative transportation methods and restarts shipments in advance. Therefore, we do not rule out the chance of a rapid decline after the price peak in the later period (around July-August), with great probability. But notice, it’s not in the moment. It is recommended to pay attention to the changes in the pan position, and the price peak needs to see a significant drop in the position.

The current stage of the market wobble is large and easy to repeat, suggesting cautious participation.

Ferroalloy: Attack manganese silicon

1.17 million lots – the highest position in history, 4.239 million lots – the highest single-day trading volume in history (weighted contracts, the same below), manganese silicon futures in April from a low of 6058 yuan/ton rose sharply to a maximum of 9154 yuan/ton, 26 trading days up 3096 yuan/ton or 51.1%, It has become another eye-catching “conspicuous package” in addition to the recent consolidated European line.

Occurrence of quotation

On 15-16 March 2024, Cyclone Meagan severely impacted operations at South32’s Groote Eylandt Mining Company (GEMCO) facility on Groote Ellant Island, Australia (later referred to as the South32 Event) and led to the suspension of operations at the mine on 18 March 2024. At the beginning of the event, the market did not pay much attention to this, on the one hand, the ship has issued a small impact on manganese ore shipments, on the other hand, the manganese silicon is really “terrible” fundamental situation – historically high inventory, sharply lower demand and still at a high supply. At the same time, the black department was in the continuous “negative feedback” after the return of the Spring Festival. From mid-March to the end of March, under the background that the black system as a whole continued to decline, the price of manganese silicon not only did not rebound under the influence of the South32 event, but continued to dip to a new low.

Subsequently, the price of manganese silicon followed the black “positive feedback” expectation to make a small repair, and there were no waves until April 17, 2024, South32 sent an email saying that GEMCO would stop shipping until at least June 2024, which affected the next day’s board slightly pulled up 1.5%. Subsequently, on April 22, 2024, South32 said in its quarterly report that it was expected to restart GEMCO terminal operations and export sales in the third quarter of fiscal year 2025, that is, the first quarter of calendar year 2025, and the outage event greatly exceeded market expectations, and the disk began to accelerate and gradually “out of control”.

Manganese silicon market drive from manganese ore end,

That is, cost drives up

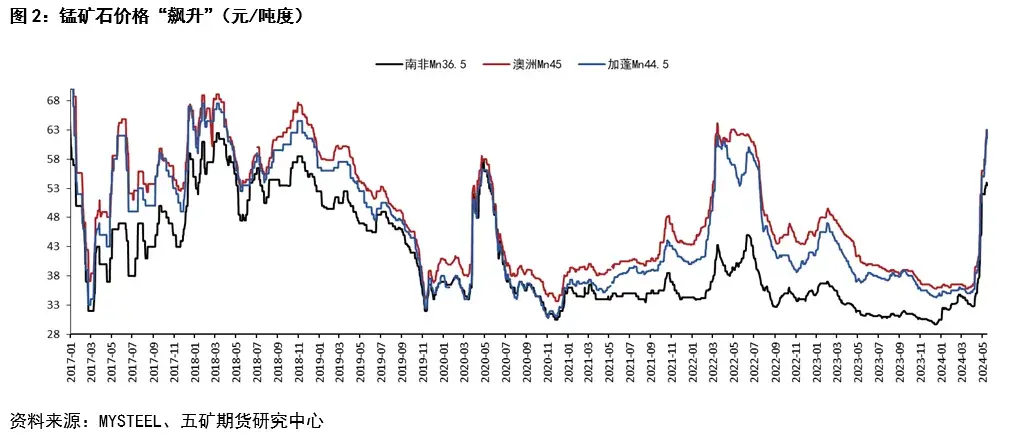

Since the South32 incident, the price of Australian manganese ore in Tianjin Port has risen from a low of 36 yuan/ton to a high of 63 yuan/ton, which is close to the high of 65 yuan/ton in 2022 and back to the level in 2019, an increase of 75%. According to the estimation of using two tons of manganese ore per ton, the equivalent production cost of manganese silicon has increased by about 2,400 yuan/ton.

The influence of the event on the import of manganese ore in China

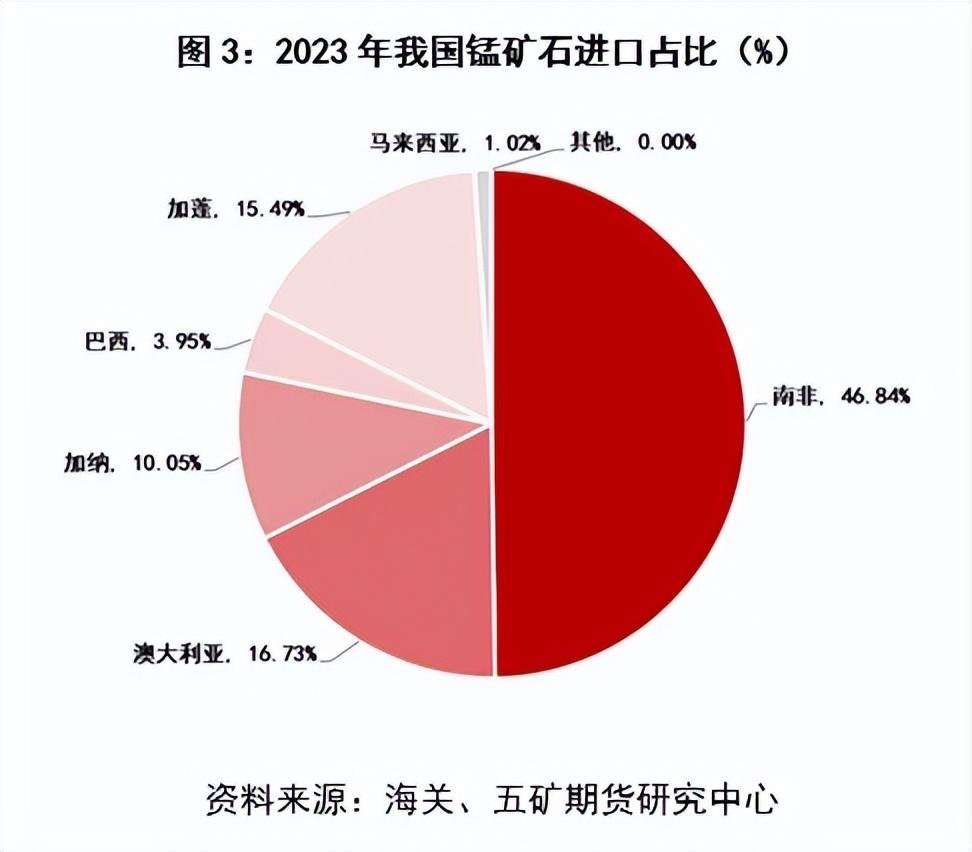

China’s largest source of manganese ore imports from South Africa, accounting for about 47%, South Africa’s ore grade is relatively low (36.5%), Australia manganese ore imports accounted for about 17% of China’s total manganese ore imports, belongs to high grade oxidation ore (42%-45%), similar to Gabon and Brazil manganese ore, the two can be used as a substitute for Australian manganese ore.

Statistics show that the global trade volume of manganese ore in 2023 is about 46.5 million tons (not converted into metal tons), of which 7.34 million tons of manganese ore was issued in Australia throughout the year, reaching 5.245 million tons in China. Approximately 76% of Australian manganese ore destined for China comes from Groot Island, with the remainder coming from Port Hedland. Considering the downward revision of South32’s production guidance by about 300,000 tons in the 2024 fiscal year, and the impact of the decline in domestic manganese silicon production on the decline in manganese ore demand, we estimate that the South32 event will affect about 300,000 tons of manganese ore imports per month, with a total impact of about 2.7-3 million tons in 9-10 months, accounting for about 10% of the total annual imports.

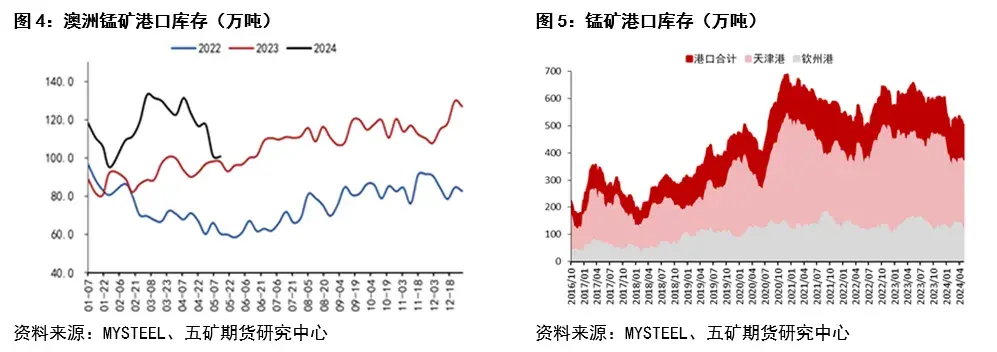

If GEMCO continues to cease operations,

The shortage of Australian ore cannot be falsified

Due to the requirement of high grade manganese ore ratio in manganese silicon production, after considering the incremental space of other production areas in the world, we find that the increase (if any) in other production areas such as Gabon, Brazil and South Africa cannot make up for the lack of supply of high grade manganese ore caused by the South32 event in the short term.

According to the calculation, under the premise of exhausting the Australian manganese ore in the port, under the optimistic situation, the inventory of the port Australian ore can meet the demand of the alloy plant before December; In the neutral case, the inventory will be exhausted around mid-September; In a pessimistic scenario, stocks will be depleted within three months. This means that the shortage of Australian ore will not be falsified in the short term until South32 takes alternative transport measures.

The supply and demand fundamentals of manganese silicon itself have not improved significantly,

Production is expected to weaken significantly year on year

Put aside the pan sentiment, return to the fundamentals of manganese silicon itself, and its supply and demand structure has not significantly improved:

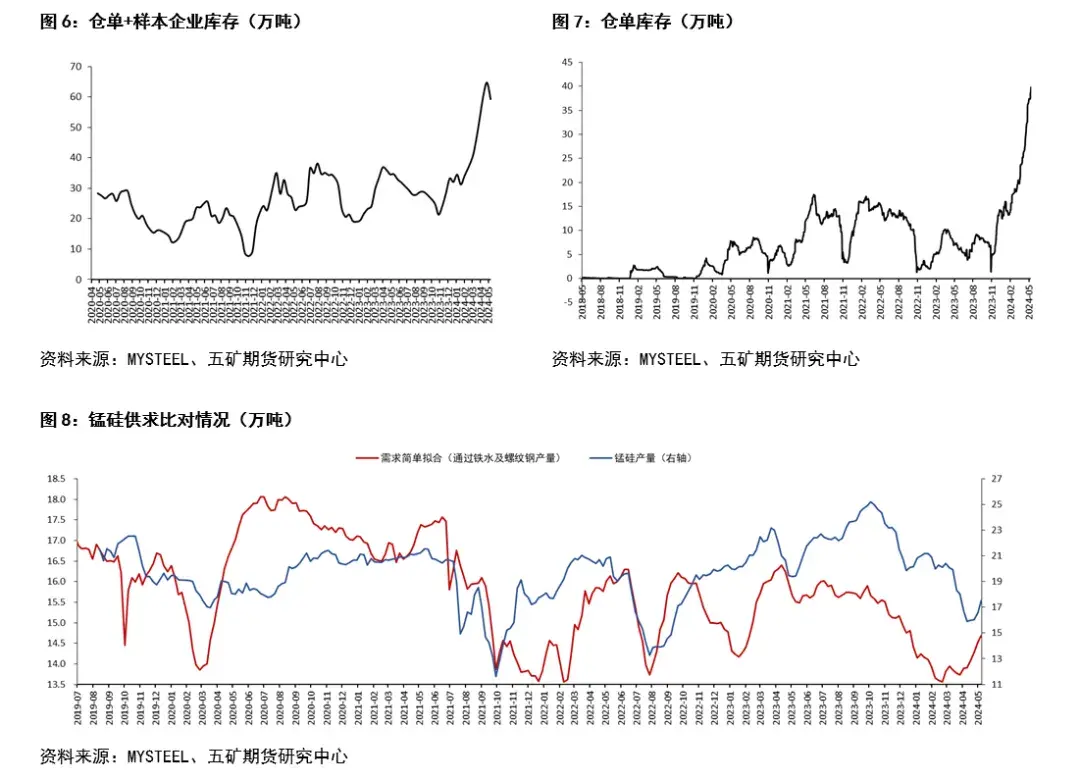

1) Historically high inventory (the dominant part is 600,000 tons, the total inventory is expected to be more than 1 million tons, the average annual output of manganese silicon in the past five years is 10.4 million tons, the output in 2023 is 11.5 million tons, and the inventory accounts for more than 10% of the annual output);

2) Supply that has started to pick up again and demand that is still relatively weak;

As of press date, from the perspective of weekly cumulative data, manganese silicon production decreased by 9.63%, hot metal production decreased by 4.69%, rebar production decreased by 20.33%, it is estimated that the cumulative decline in manganese silicon demand is about 12.5%, and the supply decline is less than the demand. And it is expected that the subsequent demand will remain low (mainly due to the significant impact of building materials under the influence of real estate).

From the perspective of demand, the supply of manganese silicon this year may also remain low, especially in the context of a high base in 2023, and it is expected that the year-on-year decline in production in 2024 is expected to reach at least 10%. If the demand is matched, the reduction needs to be more than 15%. This implies a significant reduction in the corresponding demand for manganese ore and is expected to make up for the missing amount on the supply side in terms of reduced demand.

With the industry heavily insured,

Manganese silicon spot self-reinforcing

We observe that the current spot manganese silicon is caught in a self-reinforcing “positive feedback” : After the price surge, traders continue to increase spot hedging positions, and continue to register a large number of spot into inventory orders, the current number of registered warehouse orders has accounted for about 70% of the total manifest inventory (the problem of insufficient inventory volume of the delivery warehouse is also the concern of the current shorts), coupled with the spot merchants began to sell in the face of high prices, the high inventory pressure in the early period of manganese silicon “suddenly reduced”. And this also triggered a positive spot rally.

Current market and future outlook

Since the current game is mainly in the 09 contract (recently, after the opening of the 09 contract was limited, some bulls transferred to the farther 01 contract), the multi-party will not face the pressure of receiving goods for the time being, and it is still difficult to judge when the price of manganese silicon will peak before the market sentiment has not subsided significantly (with the open position as a representative indicator).

Although there has been a continuous sharp correction after the board rose to the heavy pressure position near 9100 yuan/ton, we see that the position of the manganese silicon board remains at an absolute high level. At the same time, we observe that although the main long positions in this rally have been reduced recently, there are still a large number of net long positions in the 09 contract. Combined with the above mentioned shortage of Australian mines in the short term will not be falsified, we expect the market in the current stage or still have repeated, short-term correction may not represent the end of the market.

Considering the large spot inventory of manganese silicon (there is a centralized cancellation of the warehouse receipt in October) and poor downstream demand, bulls expect that the real willingness to receive goods is not strong (not forced). In addition, under the catalysis of high profits, it is not ruled out that South32 actively looks for alternative modes of transportation and restarts the shipment in advance (as of press date, there have been relevant rumors, although it has been proved to be false news, but under the “temptation” of high profits, it is not ruled out that it may turn into reality). Therefore, we do not rule out the chance of a rapid decline after the price peak in the later period (around July-August), with great probability. But notice, it’s not in the moment. It is recommended to pay attention to the changes in the pan position, and the price peak needs to see a significant drop in the position.

Looking back in history, the characteristics of ferroalloy varieties are always rapid high and then rapid fall, the period of high is generally 1-2 months, and the top often appears in stages of “double top”. Combined with the characteristics of the variety and the fundamentals of the variety itself, we suggest that the observation and wait for the rapid fall opportunity after the price peak, the better opportunity and participation point may appear in the first correction after the high again to confirm the fall position. The current stage of the market wobble is large and easy to repeat, suggesting cautious participation.