According to the Nihon Keizai Shimbun, the quarterly price of iron ore purchased from overseas resource companies by Nippon Steel and Japan Iron and Steel Engineering Holdings has been determined (the contract price of iron ore for Japan is determined based on the spot trading price from September to November).

In the first quarter of 2024, the FOB price (iron ore with 62% iron content) purchased by large Japanese iron mills was $113 per ton, up $10 (10%) from the price in the fourth quarter of this year.

Like China, Australia and Brazil are the main sources of iron ore for Japan. In October this year, Japan’s iron ore imports were 8.7 million tons, of which 4.5 million tons were imported from Australia and 2.8 million tons were imported from Brazil, accounting for 51.72% and 32.18% of Japan’s total iron ore imports respectively, accounting for about 83.9%.

However, unlike China, given the lack of domestic resources, Japan chose to “trade as a nation” after the war and gradually established a unified situation.

First of all, the concentration of the domestic steel industry increased rapidly, and most of it was built on the coast, and by the 1970s, five steel systems (Nippon Steel, Japan Iron and Steel Engineering Holding Company (JFE), Kobe Steel, Nippon Steel, Japan Steel (JSW)) were formed, which have been maintained to this day.

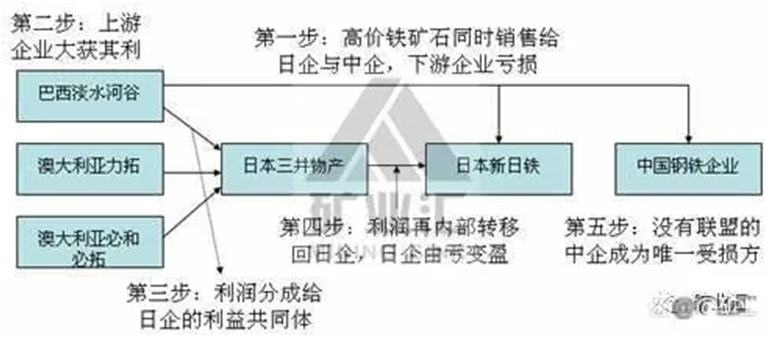

Secondly, on the trade side, the two trading companies, Mitsui & Co and Itochu Corporation, are mainly responsible for importing iron ore. Mitsui is currently one of the world’s largest iron ore shipping operators, many of China’s large steel companies are shipping merchant Mitsui, and Mitsui also invested in many steel companies, such as Japan’s largest steel mill Nippon Steel 20.1% of the equity, at the same time Mitsui is the largest steel dealer Nippon Steel. Japanese steel companies and trading houses form a community of interests,

Second, during the period 1974-2000, the interest community of the Japanese steel industry continued to increase investment in iron ore resource development projects in Australia and Brazil. Japan’s Mitsui & Co., for example, owns a stake in Brazil’s Vale, and has a combined 47 percent stake in Rio Tinto’s Robe River iron ore subsidiary – 33 percent for Mitsui, 10.5 percent for Nippon Steel and 3.5 percent for Sumitomo Metal. It holds 15% of BHP’s Newman, Yandi and Goldsworthy subsidiaries – 8% in Itochu and 7% in Mitsui, and 9% in Jimblebar subsidiaries – 4.8% in Itochu and 4.2% in Mitsui.

Japanese steel companies and trading houses have formed a community of interests in the upstream and downstream industrial chain of steel – steel companies buy overseas iron ore through trading houses, and trading houses help steel companies sell industrial products. If iron ore is expensive, the trading houses that own equity in the mines earn more and then pass the profits on to the steelmakers when they sell industrial products. If iron ore is cheaper, steel companies will make more money, and the business houses will be more profitable when they are responsible for the sale of industrial goods, forming a resource, production and trading system that allows Japanese companies to ensure profits in drought and flood.

These practices have been implemented over a long period of time and have been recognized by local governments and resource development stakeholders.

According to the World Steel Association data, from January to September 2023, the global blast furnace pig iron production of 989 million tons, an increase of 1.6%; Among them, China’s pig iron production of 678 million tons (accounting for 68.55% of global pig iron production), up 3.0%, in addition to China, overseas pig iron production of 311 million tons, down 1.3%. According to customs statistics, from January to October, China’s iron ore imports were 977 million tons, an increase of 6.4%.

The main growth country of pig iron in the world is China, and China’s iron ore demand is high, which has also caused the recent high iron ore prices. In the second half of 2023, iron ore prices as a whole are relatively strong, with the highest point reaching 135.6 US dollars/dry ton in mid-to-late November, the lowest point reaching 97.5 US dollars/dry ton in late May, and the average price at 118.4 US dollars/ton as of early December.

On the supply side, looking forward to 2024, according to incomplete statistics, the production of the four major mines is expected to increase by 9 million tons year-on-year, of which Rio Tinto’s production and sales target is raised by nearly 4 million tons, and BHP Billiton and FMG two mining companies contribute 2.5 million tons respectively. Large mining companies in major iron ore producing countries such as India, Australia, Canada and Brazil are seeking capacity expansion globally, opening new mines, building new direct reduced iron plants, pelletizing plants, etc. Based on the cornerstone plan, domestic mines will also usher in new growth drivers, and the overall supply is relatively loose.

In 2024, the recovery of the demand side will be an important basis for affecting the direction of iron ore, on the whole, the overall demand will still improve next year, but it does not rule out a phased decline. According to a number of institutions predict that the iron ore market in 2024 will show a high and low trend, and the price fluctuation range is expected to be greater than that in 2023, and the price fluctuation range of US $70-140 is expected to fluctuate.